To make it simple and understandable for everyone — economies are people doing people things. The things that people do to provide food, shelter, transportation and other needed and wanted services for themselves and their neighbors. They are living, breathing things, because they are made up of living, breathing people and they can be healthy and alive, or sick and ailing. If economies are to be healthy, each of its components need to be healthy.

There are also basically two ways to run an economy.

In one, a community produces wealth and keeps it within the community. The farmer grows the food and sells it to the local grocer. The grocer banks at the local credit union. The hospital buys its linens from a laundry/company that also provides, makes, or sells linens three miles away. The construction crew lives in the houses it builds. The factory is owned, in whole or in part, by the people who work in it, so when it has a good year, they have a good year. Money circulates. It hits the same hands two, three, four, five times before it leaves town — and then usually only to go on a vacation. That circulation is what an economy actually is.

In the other, wealth is produced locally and shipped out. A hedge fund in Manhattan buys six hundred thousand single-family homes in Phoenix, Charlotte, Atlanta, Las Vegas — houses that used to be how working families built net worth — and converts them into rental income that flows back to limited partners in New York, Miami, London, and the Gulf.

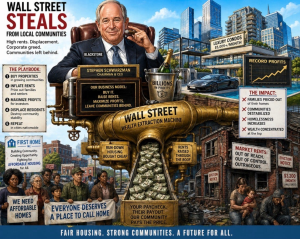

Private equity buys the nursing home, the veterinary clinic, the trailer park, the newspaper, the hospital. It takes out huge amounts of debt to do it. It then fires as many workers as possible to cut costs to show an increased bottom line, reduces services, then pays themselves huge amounts in salary and bonuses, as well as unreasonable amounts in rents after they split the land the business sits on from the business itself, placing the land into an LLC that the executives/general partners own. They then charge the hospital ungodly rents that go directly into the executives’ pockets on top of their salary and bonuses, but its hidden from the less sophisticated who do not understand they are dealing with a bunch of common thieves. In other words, they steal the company blind, they rape it, until there is nothing left to steal and then walk away, leaving the community to deal with the consequences.

The casinos on the Las Vegas Strip are owned by a real-estate trust headquartered two thousand miles away, and the rent the casino pays to operate on its own floor goes to that trust, not to anyone in Nevada. The locals get the jobs. The capital goes into the pockets of someone else far away.

That second model is what most of America live inside of now. Blackstone is the largest commercial landlord (which includes residential ownership because homes are now considered “commerical assets”) in the United States. It also owns the land under the Cosmopolitan and the Bellagio and the buildings themselves. Vici Properties owns the land under Caesars Palace, MGM Grand, the Venetian, Mandalay Bay, and most of the rest of the Strip — and the buildings where a great deal of Las Vegas’s economy actually happens — and collects rent on every square foot. The dealers, housekeepers, cooks, and valets who make the city run see almost none of that rent. It leaves. It goes to shareholders who will never set foot in Clark County and don’t care whether the schools work or the water holds out.

Call it what it is: An Extraction Economy. The town is the mine. The people are the worker bees. The wealth is the ore. And the shareholders are out of state. This is an economic model that always leads to one place only — DISASTER.

It does not have to be this way, and the evidence that it doesn’t is not theoretical. It is sitting in plain sight in places that decided, deliberately, to do something else.

Look at Catalonia. The region around Barcelona is the wealthiest part of Spain, and it has been wealthier than the Spanish average for more than a century, despite — and partly because of — a dense network of cooperatives, mutual societies, and family-owned firms that keep ownership local. Mondragón, in the Basque Country to the north, is the most famous example: a federation of worker-owned cooperatives employing roughly 70,000 people, where workers own the firm, elect the board, and share in the profits. When Mondragón does well, Mondragón’s workers do well, and the towns Mondragón sits in do well. The wealth doesn’t leave because there is nowhere else for it to go. The owners are already home. And as such, the owners have the “pride of ownership” and take care of everything. If there is a problem, they fix it immediately because its theirs, not someone else’s in a far away land. The business is maintained and operated properly by its owners which are made up of every employee there.

Look at Emilia-Romagna in northern Italy, where a third of regional GDP runs through cooperatives and the region has spent decades among the most prosperous in Europe. Look at the Mittelstand in Germany — privately held, often family-owned mid-sized manufacturers rooted in specific towns, paying skilled wages, training apprentices, and reinvesting locally — which is the actual engine of German industrial strength.

These are not folk experiments. They are the most successful regional economies in Europe, and they share a common feature: Ownership stays close to the work.

Scotland just took the boldest step yet to make this the law of the land. And my maternal grandmother was a Stewart from Scotland, whose great aunt was a woman named Mary — Queen of Scots.

In February 2026, the Scottish Parliament passed the Community Wealth Building (Scotland) Act — the first national legislation of its kind anywhere in the world. It places a legal duty on every local authority and a wide range of public bodies to plan and act around five pillars: how public money is spent, how workers are treated and paid, how land and property are used, how ownership is structured, and where finance flows. The aim, in the government’s own words, is the “generation, circulation and retention of wealth in local and regional economies.” Scottish Communities — run by Scottish ministers, who must now publish a national statement and progress reports. Councils must produce action plans. Public procurement must look first to local small businesses, social enterprises, and cooperatives. Land and property must be evaluated for community benefit, not just market price. Worker ownership and cooperative ownership are explicitly favored.

The bill grew out of a real experiment. Preston, in northern England, was a struggling post-industrial town when its council decided around 2013 to redirect its anchor institutions — the hospitals, the universities, the police, the housing associations — to buy locally wherever possible. Within a few years, tens of millions of pounds that had been leaving the local economy every year were instead circulating inside it. Preston went from one of the most deprived areas in the country to one of the most improved. Scotland watched, piloted the model in five council areas, and is now hard-wiring it into national law.

The Scottish stakes are not abstract. By the government’s own measure, the top 10 percent of Scottish households hold roughly 200 times the wealth of the bottom 10 percent. A quarter of Scots have less than a few hundred pounds in savings. The Scots looked at that and concluded that the economic model itself was the problem — that an economy designed to extract will keep extracting until there is nothing left to take — and that a different model had to be written into law before the extraction was complete.

Now Look At America

The American single-family rental market is dominated by a handful of institutional landlords who own hundreds of thousands (I believe it’s millions and they are lying) of homes between them. In some Sun Belt zip codes, corporate buyers were responsible for a majority of all home purchases at the peak. Every house they buy is a house a family cannot. Every rent check they collect is wealth that used to compound on a household balance sheet that now compounds on a hedge fund’s instead.

The first rung of the ladder by which working Americans built wealth for three generations has been sawn off and sold for parts.

In Las Vegas, the same dynamic plays out in commercial real estate. The casinos generate enormous revenue. The rent on the buildings they sit in flows to landlords in New York. The water bill — in a city running out of water — stays here. The wage bill stays here. The profit does not.

Multiply this by every city in every state in the country. Private equity now owns a meaningful share of American hospitals, nursing homes, veterinary clinics, dental practices, daycares, and local newspapers. Each acquisition follows the same pattern: cut staff, raise prices, load the acquired company with debt that is used to pay more to the General Partners. Split the land from the business, now charge the business huge rents that go into the managing partners’ pockets directly, then pay yourself huge dividends and bonuses on top of the rents, and when they businesses go bankrupt, move on. The local community keeps the consequences. The fund keeps the money.

The problem is when the business is a HOSPITAL with a quick care clinic and an emergency room, the entire community suffers and is left without a hospital and the vital services it provides. And the men who did it, should be in jail, but they are looked up to because they have a forty million dollar yacht and a home in Aspen because much of America has been fed Wall Street lies for so long they actually believe them.

This is not capitalism in any sense Adam Smith would have recognized. Smith assumed the merchant lived in the town. He assumed the owner saw the workers’ children at church. The whole moral architecture of his economics rested on proximity. Strip out proximity and you do not get a freer market. You get a more efficient extraction tool.

So what would a wealth-creation economy actually look like in an American city — say, the one I happen to live in Las Vegas?

Do What Scotland Just Did!

Let’s start with housing. The first thing I would suggest is anytime you hear a person say “Work Force Housing” — look at them with a great deal of distain, and say “Fuck You, you arrogant fuck” and then stomp on the arch of their foot really hard with the heal of your shoe and hopefully you break at least one bone. I’m kidding. That would be assault, but you get the point I am trying to make. The mere utterance of such a statement is, by itself, an attempt to create “classes” of people — to separte and divide people as if the “Work Force” is less valuable than the so called “Ruling Class” who own the casinos and the land they sit on and who allow the CEOs running the casinos to pay themselves 400 times what they pay their employees. The casinos would operate much more effectively if every employee had ownership in the business and had a say in how they were run.

The next thing any city or state could and should do in such a situation is pass a City or State Ordinance that places a massive tax on any company that owns more than 50 homes in the City. An extra $5,000 on every $100,000 of value. Then give them a certain amount of time to sell off every home they own above 50 (no more than five years). And they cannot purchase another one, or every home they own is taxed another $5,000 on every $100,000 of value. I could almost guarantee that suddenly there would be lots of affordable homes in Las Vegas that working people could afford.

Extremely strong rent controls should also be instituted so working people who do rent can enjoy their lives. Happy people are far more productive than people who are constantly worried about paying the rent and having the price of everything go up, except their salaries.

Ownership of Housing. The wealth of most Americans has come from equity in the homes they have owned over time. Now that wealth is going to a small group of Private Equity Funds and Reits. This weakens our communities and the local economies. Besides doing what was suggested above, a community should pass laws and ordinances to encourage the use of local banks and credit unions. And encourage those same institutions to provide mortgages for local housing to create low-cost mortgages, by having cities, counties and states underwrite housing bonds to provide such mortgages, which would keep things affordable and the wealth within the local communities, counties and states rather than sending it to Wall Street. The wealth of the community would then stay within the community. This would make our communities, states, and country much stronger. Each of the parts making up the economy would be stronger and healthier making the whole healthier.

Distressed commercial buildings — the half-empty office towers nobody knows what to do with — get converted to affordable apartments, owned by entities structured to keep them affordable, with residents who can buy in overtime and build equity rather than just pay rent forever. (Understanding that very few commercial buildings can be converted into residential housing. They are simply not laid out right to allow for the necessary plumbing, etc. to be built out as it needs to be for an economical price and sometimes not structurally). The mortgage payments (or rents in some situations) would stay in the community and state by doing what was describe earlier with mortgages. (This is the thesis of the Fund I am building. I am not pretending I am a neutral observer.) This way the money doesn’t flow to a New York Hedge Fund who is trying to suck as much money as they possibly can from the tenants.

Procurement. The hospital, the school district, the university, the city government, the convention authority — between them they spend billions a year. Right now, most of it leaves. Direct even half of it toward local suppliers, local contractors, local food producers, local cooperatives, and you have transformed the local economy without raising a single tax.

Stop the Extraction of Billions in Student Loans. Over the years, Wall Street has bribed state regents to raise tuitions by tens of thousands of dollars making getting an education extremely expensive. The result has been that young people have been forced to borrow tens of thousands of dollar to attend school. I wrote bill to fix solve that which can be read here. slfla.org. It would give employer’s tax credits if they pay off the students loans

Business Ownership. Don’t allow monopolies to be created or exist. Make it cheaper and easier for retiring small-business owners (or large business owners) — and there are millions of baby-boomer owners about to retire with no succession plan — to sell to their employees through ESOPs (Employee Stock Ownership Plans) and worker cooperatives instead of to private equity roll-ups. The federal tax code already gives ESOPs significant advantages. State and local policy can do far more. When the owner of the local HVAC company retires, the question of who buys it is the question of where the next twenty years of that company’s profits will go or if the business will just go away. Cities and counties should write ordinances that encourage and help small businesses find others in the community to buy such businesses (including funding for employee ownership) that will keep the business operating and ownership within the the community when such things happen. When the City or County puts bids out for whatever type of work that needs to be done, the first rights to bid on such things should be given to local people and businesses wherever possible and not to large national funds or companies until local options have been given the opportunity to participate.

In Las Vegas, Private Equity and other such funds not only own all of the land on the Strip and charge outrageously high rents, which is why everything costs so much on the Strip, which is why no one wants to come to Vegas anymore, but they also own almost every home that isn’t owned by the people living in it. Such funds own almost every strip mall and every other business in the City. They own the HVAC businesses, the hospitals, the veterinary clinics, the restaurants, the fast food places and on and on, and if they don’t own a small business, they drive tens of thousands of them out of business by charging such high amounts of rents for the spaces needed to operate such a business. The high rents also make it next to impossible for a small business to get started and off its feet. The high rents suck all of the profits the company makes out of the owner’s pockets and into the fund’s pockets in New York or whereever they are located at a time when the owners need as much capital as they can get to get their new business up and running. And every dime of the high rents leaves the community, which weakens it even more. This will never change until local leaders wakeup to the fact that these big funds are not their friends and by allowing them to own everything, the local economies keep getting weaker, not stronger. They are people who do not care at all about the local community or the local economy.

Finance. Public deposits — city money, county money, pension money — sitting in large money-center banks that lend it back into corporate debt and securitized rentals extracts money from local communities. Move the majority of it into community banks, credit unions, and CDFIs (Community Development Financial Institutions) that lend to local businesses and local borrowers. Same dollars. Different gravity and outcomes.

None of this is Socialism. None of it is novel. The Catalans and Basques and Emilians and Germans have been doing it for a century. The Scots just made it law. America was founded on this model and became the greatest country and economy in the world. Doing it is Smart Economics. It has only changed since we allowed the Too Big To Fail Banks to exist and we bailed them out. Doing that was not a good thing and has led to the horrible malaise of unaffordability we now face and has weakened the American Economies immensely.

Of course, the objections will come, and it always comes from the same direction. You can’t tell capital where to go. You’ll scare off investment. The market knows best. Fuck such nonsense.

The market does not know best. The market knows where the highest extractable yield is, and right now that yield is in turning American homes into rental cash flow, American hospitals into debt-laden roll-ups, and American downtowns into rent-collection schemes for absentee owners. That is not the invisible hand. That is a very visible hand, attached to a very specific arm, reaching into very specific pockets — yours, and your neighbors’, and your kids’.

And make Lina Khan the head of the FTC again and let her do her job.

A community has every right to decide that the wealth it produces will, to the greatest extent possible, stay where it was produced. That is not a radical proposition. That is the proposition every functional economy in human history has rested on. The radical proposition — historically novel, historically destructive — is the one we are living under now: That an economy exists to be drained for the benefit of people who do not live in it and who think it is their right to rule.

Scotland chose. Catalonia chose, generations ago. Preston chose. Mondragón chose.

We as Americans have still not yet chosen. But we will, one way or the other. Either we say no to the Wall Street thieves and tell them that Enough Is Enough and then build the institutions — the funds, the cooperatives, the community banks, the procurement rules, the ownership structures — that keep wealth circulating where it is made, or we wake up in twenty years and discover that everything we built has been quietly retitled in someone else’s name.